In partnership with Going Places by Malaysia Airlines

At the LEAP Summit in November last year, TM One Chief Executive Officer (CEO), Ahmad Taufek Omar said: “Every disruption pivots on creativity – a new vision, a new insight of how technology can uplift people and their goals onto a more agile, faster path.”

His words could not have been more prescient for the disruption that followed just a couple of months later, when the Covid-19 pandemic swept the globe, sending industries scrambling to regain their footing.

Nearly a year since the summit, though the dust remains unsettled, the vision, insight and technology he alluded to are on clear display in the business world. Quite simply, there is a cultural shift underway, and there is already a lot that businesses can do – culturally and technologically – to become more resilient in a changing world.

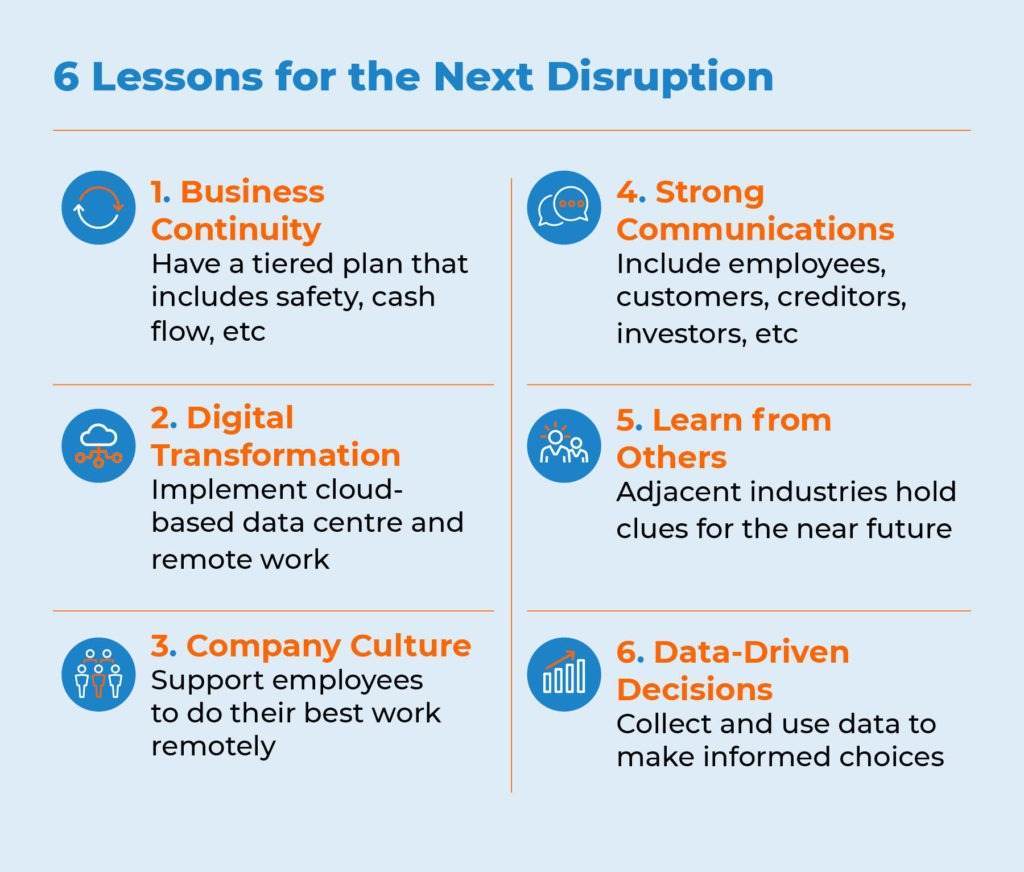

Analyst firms such as Omdia (formerly Ovum) expects Malaysian businesses will view the pandemic as a catalyst to sharpen their business continuity measures and change the way they do business. Ideally, enterprises should have a specific pandemic-focused business continuity plan (BCP) already prepared, says the Omdia report, but – as an alternative – repurposing an existing one that covers “civic emergencies” should suffice.

“The plan should incorporate a tiered response, clearly identifying the actions to be taken at each level and the circumstances that would trigger implementation of the next level,” notes the report.

Professional services network EY elaborated on the requirements of a strong BCP in a March 2020 report, highlighting the need for employee health and safety, short-term liquidity, knowledge of government support measures and many other operational details.

The ability to work effectively and safely away from the office is a key aspect of business continuity and stability, as it is the ability to meet fluctuations in customer demand resulting from any disruption.

There have been a few reports of organisations experiencing big jumps in traffic during Malaysia’s Movement Control Order (MCO) period earlier this year, putting strain to their network and resources, and necessitating an overnight infrastructure upgrade.

Rather than waiting for another disruption, companies can be better prepared by moving data centres and other operations to the cloud and introducing remote meeting and file-sharing applications into their daily operations.

While there is a need for digital transformation, it must go hand-in-hand with a shift in company culture. A recent survey by productivity software company Wrike found that 49% of workers have never worked from home. Not only is there a generational difference around attitudes towards working remotely, there is a lack of consensus around manager expectations, best team practices, efficient software and suitable IT infrastructure.

But the new paradigm of working remotely will become mainstream and attitudes must catch up. Ahmad Taufek also commented on the cultural changes required for digitalisation during an interview last year, "Culture is a critical factor underlying a successful transformation. Companies, whether they are big or small, must be ready to change their mindsets to stay relevant and to adapt to the new order of the economy."

All the appropriate technologies, and cloud infrastructure services are already on hand to ensure companies can operate from both home and the office. It is now a matter of implementation well ahead of the next disruption.

As part of its 2019 Global Crisis Survey, consulting firm Pricewaterhouse Coopers (PwC) found that companies are able to not only survive in times of crisis, but also emerge even stronger in the aftermath, as a result of being prepared and having effective stakeholder communications.

This communication must be regular, transparent and far-reaching, relaying not just evolving company policies but also relevant government guidelines. Furthermore, it must extend beyond immediate employees, and include customers, suppliers, creditors and investors, just to name a few.

According to American customer service software company Zendesk’s Benchmark Snapshot, of the 23,000 companies that use their services, the three biggest industries that have seen spikes in support requests since late February are restaurants, grocery brands and remote work & learning.

Companies in the same or adjacent industries can glean a great deal of useful information from successes in these three areas, particularly in terms of the digital transformations implemented this year.

Disruptions are times for quick-thinking and fast decisions, but that doesn’t mean company leadership should shoot form the hip. The PwC survey also found that companies become stronger when supported by data-driven decision making.

Having a big data initiative in place ensures that businesses can respond effectively and swiftly, based on dynamically evolving set of data. The ability to make fast and well-informed business decisions is yet another reason why digital transformations – and the resulting collection of relevant data – can yield benefits well into the next disruption.

As Malaysia’s digital enabler for enterprises and public sector, TM One has played its role in helping customers to weather challenges whenever and wherever required, and this has been especially true during the Covid-19 pandemic.

Through its Cloud Alpha service, TM One supports infrastructure, platform and software needs. That means companies can implement everything from remote servers and collaboration and file-sharing platforms, as well as big data gathering, expanding as their needs grow, and with 24/7 IT support.

Covid-19 has been a once-in-a-generation disruption to lives and businesses. But it has prompted innovation, preparedness and digital transformation across all sectors. In Malaysia, it has kick started a new digital revolution that will ensure better resiliency in the years and generations to come.

For more information on how to begin a digital transformation for your company, please visit TM One’s Cloud Alpha service website.