I’ve moderated and sat in a fair number of fintech panel discussions over the years, a question that is brought up 9 out of 10 in every discussion is “What do you think are the key technology shaping fintech and banking in Malaysia?” and some variation of that same question.

If you’re like me who have attended too many fintech conferences, the answers will come as no surprise to you. The common answers are often; blockchain, artificial intelligence, open banking, virtual banking, and mobile payment.

Yet despite the importance of electronic Know Your Customer or eKYC and digital identity, very rarely you will hear any panellists in these conferences pointing out the impact of eKYC and digital identity in Malaysia’s banking and fintech ecosystem.

A study conducted by Mckinsey shows that there is a potential cost reduction of 90% in customer onboarding cost by enabling eKYC. The same study also indicated that digital identity could potentially enable 1.7 billion of the unbanked population to gain access to financial services.

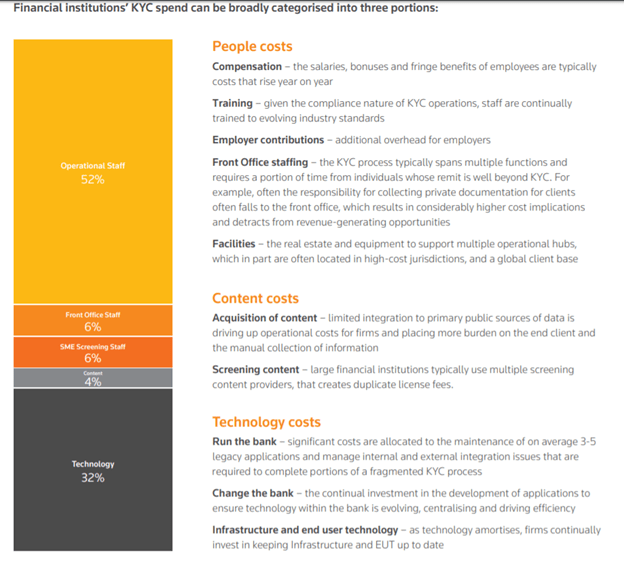

A separate study by Refinitiv further breaks down the cost of KYC, much of the cost is largely attributed to staffing costs, which supports the idea that digitising the KYC process could significantly reduce the cost of customer onboarding.

It is a fact that has not gone unnoticed by Bank Negara Malaysia, in 2017 the regulator issued the eKYC framework for remittance companies and subsequently in 2019, a similar draft was issued for money changers.

Though there is development particularly within the Money Services Business (MSB) space, the regulator has not made any formal announcement on eKYC guidelines for the wider financial services sector.

There have been some nuggets of information though, during the MyFintech Week earlier this year, BNM’s financial development and innovation department director Suhaimi Ali mentioned that there are currently 11 banks trialing eKYC solutions.

Suhaimi did not disclose further the nature of the trial nor the details of the provider but credit reporting agency CTOS who is also present at the event shared in a separate session that they are trialing their eKYC project with several banks and they are looking to enter Bank Negara Malaysia sandbox.

Meanwhile, Muhammad Ghadaffi Mohd Tairobi, the Vertical Director for Banking, Financial Services & Insurance of TM One acknowledges that there are many benefits of Digital ID from a business perspective, as it will save time and money by reducing it to over the counter transactions, increasing productivity and enabling seamless and digital driven experiences for customers. He believes that eKYC then becomes an important process for the banks to perform customer on-boarding faster compared to traditional way of over the counter.

However, Ghadaffi’s key concern was on managing digital ID fraud. He said “This is why TM One eKYC solution is in compliant with Risk Management in Technology (RMiT) and Data Residency and Sovereignty requirements to assist the BFSI industry in the successful implementation of this initiative”.

Written by: Vincent Fong, Fintech News